impulse

Generate regression model with ARIMA errors impulse response function (IRF)

Description

y = impulse(Mdl)impulse returns the dynamic responses starting at period 0,

during which impulse applies a unit shock to the

innovation.

impulse(___) plots a discrete stem plot of the IRF of

the input regression model with ARIMA errors to the current axes, using any of the input

argument combinations in the previous syntaxes.

impulse(

plots on the axes specified by ax,___)ax instead of

the current axes (gca). ax can precede any of the input

argument combinations in the previous syntaxes. (since R2024a)

[___, plots the IRF and additionally returns handles to the plotted graphics objects. Use elements of h]

= impulse(___)h to modify properties of the plot after you create it. (since R2024a)

Examples

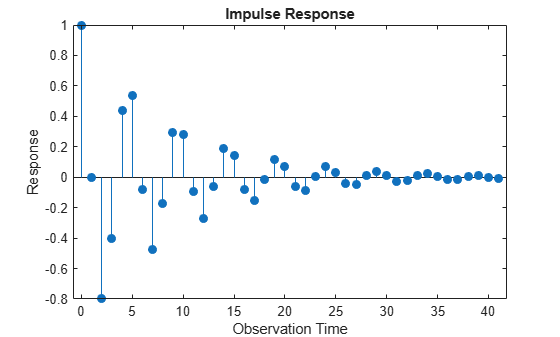

Specify the following regression model with ARMA(2,1) errors:

where is Gaussian with variance 0.1.

Mdl = regARIMA(Intercept=0,AR={0.5 -0.8},MA=-0.5, ...

Beta=[0.1; -0.2],Variance=0.1);Time the calculation of and plot the impulse response function without specifying the number of observations.

impulse(Mdl)

The model is stationary; the impulse response function decays in a sinusoidal pattern.

Specify the following regression model with ARMA(2,1) errors:

where is Gaussian with variance 0.1.

Mdl = regARIMA(Intercept=0,AR={0.5 -0.8},MA=-0.5, ...

Beta=[0.1; -0.2],Variance=0.1);Store the impulse response function for 15 periods.

y = impulse(Mdl,15)

y = 15×1

1.0000

0

-0.8000

-0.4000

0.4400

0.5400

-0.0820

-0.4730

-0.1709

0.2930

0.2832

-0.0928

-0.2729

-0.0623

0.1872

The length of the output impulse response series is numObs. y(1) is the IRF at period 0, during which impulse shocks Mdl. y(15) is the IRF at period 14.

Input Arguments

Output Arguments

More About

Tips

To improve performance of the filtering algorithm, specify the number of observations,

numObs, to include in the impulse response.

Algorithms

If you specify the number of periods

numObs,impulsecomputes the IRF by filtering a unit shock followed by an appropriate length vector of zeros. The filtering algorithm is very fast and results in an IRF ofnumObslength.If you do not specify

numObs,impulseimplements this procedure:Convert the error model to a pure moving average (MA) polynomial by using the relatively slow lag operator polynomial division algorithm.

Truncate the pure MA polynomial according to default tolerances because the polynomial is generally of infinite degree.

This procedure produces an IRF of generally unknown length. For more details, see

LagOpandmldivide.

References

[1] Box, George E. P., Gwilym M. Jenkins, and Gregory C. Reinsel. Time Series Analysis: Forecasting and Control. 3rd ed. Englewood Cliffs, NJ: Prentice Hall, 1994.

[2] Enders, Walter. Applied Econometric Time Series. Hoboken, NJ: John Wiley & Sons, Inc., 1995.

[3] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

[4] Lütkepohl, Helmut. New Introduction to Multiple Time Series Analysis. New York, NY: Springer-Verlag, 2007.