parcorr

Sample partial autocorrelation

Syntax

Description

[

returns the sample partial autocorrelation function

(PACF) and associated lags of the input univariate time series data.pacf,lags] = parcorr(y)

PACFTbl = parcorr(Tbl)DataVariable name-value argument. (since R2022a)

[___,

uses any input-argument combination in the previous syntaxes, and returns the

output-argument combination for the corresponding input arguments and the approximate

upper and lower confidence bounds bounds]

= parcorr(___)bounds on the PACF.

[___] = parcorr(___,

uses additional options specified by one or more name-value arguments. For example,

Name=Value)parcorr(Tbl,DataVariable="RGDP",NumLags=10,NumSTD=1.96) returns 10

lags of the sample PACF of the table variable "RGDP" in

Tbl and 95% confidence bounds.

parcorr(___) plots the sample PACF of the input

series with confidence bounds.

parcorr(

plots on the axes specified by ax,___)ax instead of

the current axes (gca). ax can precede any of the input

argument combinations in the previous syntaxes.

[___, plots the sample PACF of the input series and

additionally returns handles to plotted graphics objects. Use elements of

h]

= parcorr(___)h to modify properties of the plot after you create it.

Examples

Compute the PACF of a univariate time series. Input the time series data as a numeric vector.

Load the quarterly real GDP series in Data_GDP.mat. Plot the series, which is stored in the numeric vector Data.

load Data_GDP

plot(Data)

The series exhibits exponential growth.

Compute the returns of the series.

ret = price2ret(Data);

ret is a series of real GDP returns; it has one less observation than the real GDP series.

Compute the PACF of the real GDP returns, and return the associated lags.

[pacf,lags] = parcorr(ret); [pacf lags]

ans = 21×2

1.0000 0

0.3329 1.0000

0.0828 2.0000

-0.1205 3.0000

-0.1080 4.0000

-0.0869 5.0000

0.0226 6.0000

-0.0254 7.0000

-0.0243 8.0000

0.0699 9.0000

0.0143 10.0000

-0.0390 11.0000

-0.2032 12.0000

-0.0513 13.0000

0.0154 14.0000

⋮

Let be the real GDP return at time t. pacf(3) = 0.0828 means that the correlation between and , after adjusting for the linear effects of on , is 0.0828.

Since R2022a

Compute the PACF of a time series, which is one variable in a table.

Load the electricity spot price data set Data_ElectricityPrices.mat, which contains the daily spot prices in the timetable DataTimeTable.

load Data_ElectricityPrices.mat

DataTimeTable.Properties.VariableNamesans = 1×1 cell array

{'SpotPrice'}

Plot the series.

plot(DataTimeTable.SpotPrice)

The time series plot does not clearly indicate an exponential trend or unit root.

Compute the PACF of the raw spot price series.

PACFTbl = parcorr(DataTimeTable)

PACFTbl=21×2 table

Lags PACF

____ ________

0 1

1 0.5541

2 0.10938

3 0.099833

4 0.029511

5 0.038836

6 0.065892

7 0.029965

8 0.034951

9 0.050091

10 0.051031

11 0.033994

12 0.051877

13 0.028973

14 0.047456

15 0.11895

⋮

parcorr returns the results in the table PACFTbl, where variables correspond to the PACF (PACF) and associated lags (Lags).

By default, parcorr computes the PACF of the last variable in the table. To select a variable from an input table, set the DataVariable option.

Since R2022a

Consider the electricity spot prices in Compute PACF of Table Variable.

Load the electricity spot price data set Data_ElectricityPrices.mat. Compute the PACF and return the PACF confidence bounds.

load Data_ElectricityPrices

[PACFTbl,bounds] = parcorr(DataTimeTable)PACFTbl=21×2 table

Lags PACF

____ ________

0 1

1 0.5541

2 0.10938

3 0.099833

4 0.029511

5 0.038836

6 0.065892

7 0.029965

8 0.034951

9 0.050091

10 0.051031

11 0.033994

12 0.051877

13 0.028973

14 0.047456

15 0.11895

⋮

bounds = 2×1

0.0532

-0.0532

Assuming the spot prices follow a Gaussian white noise series, an approximate 95.4% confidence interval on the PACF is (-0.0532, 0.0532).

Since R2022a

Load the US quarterly macroeconomic series data Data_USEconModel.mat. Remove all missing values from the timetable of data DataTimeTable by using listwise deletion.

load Data_USEconModel

DataTimeTable = rmmissing(DataTimeTable);Compute the PACF of the raw effective federal funds rate FEDFUNDS by using the OLS method (the default method when the data does not contain any missing values). Change the name of the PACF variable of the output table to ols.

PACFTbl = parcorr(DataTimeTable,DataVariable="FEDFUNDS",Method="ols"); PACFTbl = renamevars(PACFTbl,"PACF","ols");

Compute the PACF of the raw effective federal funds rate FEDFUNDS by solving the Yule-Walker equations. Store the result as the variable yw in PACFTbl.

PACFTbl.yw = parcorr(DataTimeTable.FEDFUNDS,Method="yule-walker");Compare the PACFs between the methods.

PACFTbl

PACFTbl=21×3 table

Lags ols yw

____ _________ _________

0 1 1

1 0.92881 0.91502

2 0.074551 0.061337

3 0.14949 0.15031

4 -0.23745 -0.20808

5 0.073346 0.073911

6 -0.25854 -0.21128

7 0.021783 0.018625

8 0.10817 0.092159

9 0.16147 0.10987

10 -0.081344 -0.077452

11 0.050378 0.034769

12 0.075574 0.070003

13 0.026074 0.02403

14 -0.036989 -0.025924

15 0.074656 0.048657

⋮

Plot the PACFs in the same stem plot.

stem(repmat(PACFTbl.Lags,1,2),PACFTbl{:,["ols" "yw"]},"filled")

title("PACF of Effective Federal Funds Rate")

legend(["OLS" "Yule-Walker"])

Specify the AR(2) model:

where is Gaussian with mean 0 and variance 1.

rng(1); % For reproducibility

Mdl = arima(AR={0.6 -0.5},Constant=0,Variance=1)Mdl =

arima with properties:

Description: "ARIMA(2,0,0) Model (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

P: 2

D: 0

Q: 0

Constant: 0

AR: {0.6 -0.5} at lags [1 2]

SAR: {}

MA: {}

SMA: {}

Seasonality: 0

Beta: [1×0]

Variance: 1

Simulate 1000 observations from Mdl.

y = simulate(Mdl,1000);

Plot the PACF. Specify that the series is an AR(2) process.

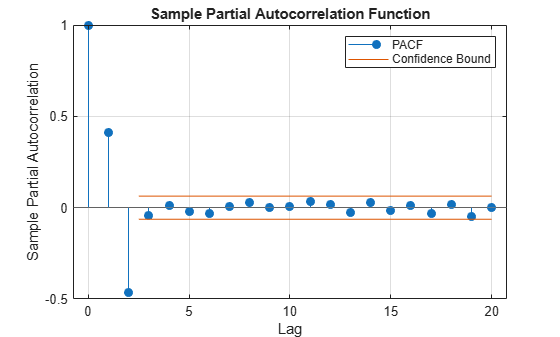

parcorr(y,NumAR=2)

The PACF cuts off after the second lag. This behavior indicates an AR(2) process.

Specify the multiplicative seasonal ARMA model:

where is Gaussian with mean 0 and variance 1.

Mdl = arima(AR={0.75 0.15},SAR={0.9 -0.75 0.5}, ...

SARLags=[12 24 36],MA=-0.5,Constant=2, ...

Variance=1);Simulate data from Mdl.

rng(1); y = simulate(Mdl,1000);

Plot the default partial autocorrelation function (PACF).

figure parcorr(y)

The default correlogram does not display the dependence structure for higher lags.

Plot the PACF for 40 lags.

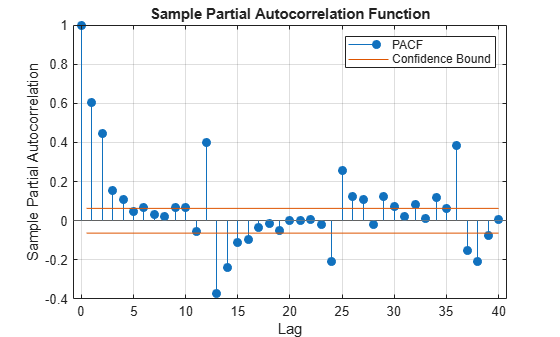

figure parcorr(y,NumLags=40)

The correlogram shows the larger correlations at lags 12, 24, and 36.

Input Arguments

Name-Value Arguments

Output Arguments

More About

Tips

To plot the PACF without confidence bounds, set

NumSTD=0.

Algorithms

parcorr plots the PACF when you do not request any output or when

you request the fourth output h.

References

[1] Box, George E. P., Gwilym M. Jenkins, and Gregory C. Reinsel. Time Series Analysis: Forecasting and Control. 3rd ed. Englewood Cliffs, NJ: Prentice Hall, 1994.

[2] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.