archtest

Engle test for residual heteroscedasticity

Syntax

Description

h = archtest(res)

StatTbl = archtest(Tbl)DataVariable name-value argument.

[___] = archtest(___,

specifies options using one or more name-value arguments in

addition to any of the input argument combinations in previous syntaxes.

Name=Value)archtest returns the output argument combination for the

corresponding input arguments.

Some options control the number of tests to conduct. The following conditions apply when

archtest conducts multiple tests:

For example, archtest(Tbl,DataVariable="ResidualGDP",Alpha=0.025,Lags=[1

4]) conducts two tests, at a level of significance of 0.025, for the presence of

heteroscedasticity in the variable ResidualGDP of the table

Tbl. The first test includes 1 lag in the AR model

of the squared residuals, and the second test includes 4 lags.

Examples

Test a time series for ARCH effects using default options of archtest. Input the time series data as a numeric vector.

Load the Deutschmark/British pound foreign-exchange rate data set.

load Data_MarkPoundData is a time series vector of daily Deutschmark/British pound bilateral spot exchange rates.

Plot the series.

plot(Data) title("\bf Deutschmark/British Pound Bilateral Spot Exchange Rate") ylabel("Spot Exchange Rate") xlabel("Business Days Since January 2, 1984")

The series appears nonstationary.

To stabilize the series, convert the spot exchange rates to returns.

returns = price2ret(Data); plot(returns) title("\bf Deutschmark/British Pound Bilateral Spot Exchange Rate") ylabel("Return") xlabel("Business Days Since January 3, 1984")

Compute the deviations of the return series from the mean.

residuals = returns - mean(returns);

At 0.05 level of significance, test the residual series of the returns for lag 1 ARCH effects.

h = archtest(residuals)

h = logical

1

The result h = 1 indicates rejection of the null hypothesis of no conditional heteroscedasticity in favor of a significant lag 1 ARCH effect in the return series.

Load the Deutschmark/British pound foreign-exchange rate data set.

load Data_MarkPoundPreprocess the data by following this procedure:

Stabilize the series by computing daily returns.

Compute the deviations from the mean return.

returns = price2ret(Data); residuals = returns - mean(returns);

Test the residual series for a significant lag 1 ARCH effect. Return the test decision, -value, test statistic, and critical value.

[h,pValue,stat,cValue] = archtest(residuals)

h = logical

1

pValue = 0

stat = 96.2379

cValue = 3.8415

Test a time series, which is one variable in a table, for ARCH effects using default options of archtest.

Load the equity index data set Data_EquityIdx. Preprocess the daily NASDAQ closing prices by performing the following actions:

Convert the price series to a percentage return series by using

price2ret.Represent the series as residuals that fluctuate around a constant level by centering the returns series.

Store the residual series in the table with the rest of the data. Because the price-to-return conversion reduces the sample size from the head of the series, impute the missing residual with the first residual.

load Data_EquityIdx

ret = 100*price2ret(DataTable.NASDAQ);

res = ret - mean(ret);

DataTable.Residuals_NASDAQ = [res(1); res];

DataTable.Properties.VariableNames{end}ans = 'Residuals_NASDAQ'

The residual series is the last variable in the table.

Conduct the Engle's ARCH test on the residuals series at a 5% significance level by supplying the entire data set archtest.

StatTbl = archtest(DataTable)

StatTbl=1×6 table

h pValue stat cValue Lags Alpha

_____ ______ _____ ______ ____ _____

Test 1 true 0 208.1 3.8415 1 0.05

archtest returns test results and settings in the table StatTbl, where variables correspond to test results (h, pValue, stat, and cValue) and settings (Lags and Alpha), and rows correspond to individual tests (in this case, archtest conducts one test).

h = 1 and pValue = 0 rejects the null hypothesis and suggests that the evidence for ARCH(1) conditional heteroscedasticity in the NASDAQ returns residual series is strong.

By default, archtest tests the last variable in the table. To select a variable from an input table to test, set the DataVariable option.

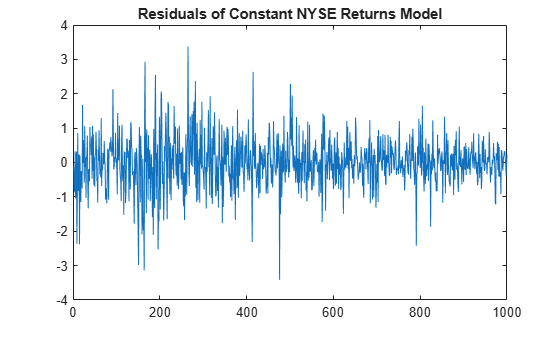

Conduct several, separate ARCH tests that use different significant levels. Consider the first 1000 days of the daily NYSE closing prices in the equity index data set from Conduct Engle's ARCH Test on Table Variable. Test a time series, which is one variable in a table, for ARCH effects using default options of archtest.

Load the time series data and consider the first 1000 observations. Preprocess and compute the residuals of the NYSE series from a constant only model.

load Data_EquityIdx

T = 1000;

DataTable = DataTable(1:T,:);

ret = 100*price2ret(DataTable.NYSE);

res = ret - mean(ret);

DataTable.Residuals_NYSE = [res(1); res];Plot the residuals of the NYSE percent returns series.

plot(1:T,DataTable.Residuals_NYSE)

title("Residuals of Constant NYSE Returns Model")

The first half of the series appears to have a larger variance than the latter half, which can indicate the presence of volatility clustering.

Conduct the Engle's ARCH test on the residuals series at a 10%, 5%, 1%, and 0.1% significance levels. Specify the table variable name of the residuals.

StatTbl = archtest(DataTable,Alpha=[0.1 0.05 0.01 0.001],DataVariable="Residuals_NYSE")StatTbl=4×6 table

h pValue stat cValue Lags Alpha

_____ _________ ______ ______ ____ _____

Test 1 true 0.0058387 7.5994 2.7055 1 0.1

Test 2 true 0.0058387 7.5994 3.8415 1 0.05

Test 3 true 0.0058387 7.5994 6.6349 1 0.01

Test 4 false 0.0058387 7.5994 10.828 1 0.001

The output table StatTbl contains a row for each test. The test rejects the null hypothesis for each significance level except 0.1% (pValue is the lowest significance level you can use to reject the null hypothesis).

To draw valid inferences from Engle's ARCH test, determine a suitable number of lags for the model by following this procedure:

Fit the model over a range of plausible lags.

Compare the information criteria of the fitted models.

Choose the number of lags that yields the best fitting model for the ARCH test.

Load and Process Data

Load the equity index data set Data_EquityIdx. Convert the table of data DataTable to a timetable.

load Data_EquityIdx dates = datetime(dates,"ConvertFrom",'datenum'); TT = table2timetable(DataTable,RowTimes=dates); TT.Dates = [];

TT is a timetable containing the same data variable as DataTable, but observations (rows) are associated with the closing times in dates.

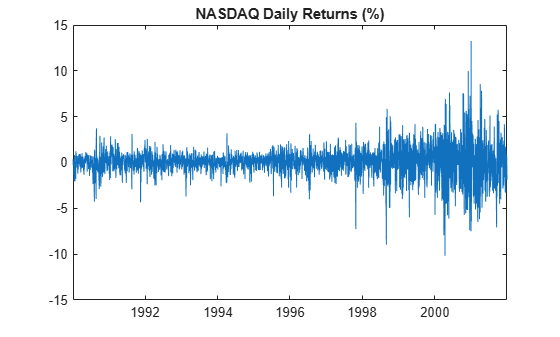

Preprocess the daily NASDAQ closing prices by performing the following actions:

Convert the price series to a return series by using

price2ret.The sampling rate has a relatively high frequency. Therefore, the daily changes can be small. For numerical stability, scale the data by 100.

Store the percent returns series in the table with the rest of the data. Because the price-to-return conversion reduces the sample size from the head of the series, prepend the series with the first percent return.

ret = 100*price2ret(TT.NASDAQ);

TT.Returns_NASDAQ = [ret(1); ret];

TT.Properties.VariableNames{end}ans = 'Returns_NASDAQ'

Plot the percent returns series.

figure

plot(TT.Time,TT.Returns_NASDAQ)

title("NASDAQ Daily Returns (%)")

The series appears to fluctuate at a constant level. The last quarter of the residual series seems to have higher variance than the first three quarters. This volatile behavior indicates conditional heteroscedasticity.

Fit ARCH Models Over Grid of Lags

Fit an ARCH() model to the NASDAQ percent returns for each . Store the loglikelihood of each fit.

numLags = 4; logL = zeros(numLags,1); % Preallocation for k = 1:numLags Mdl = garch(0,k); [~,~,logL(k)] = estimate(Mdl,TT.Returns_NASDAQ,Display="off"); end

Determine Suitable Number of Lags for Test

Determine the best fitting model by computing and comparing each AIC. Choose the number of lags for the test that corresponds to the best fitting model.

aic = aicbic(logL,1:numLags); [~,lags] = min(aic)

lags = 4

The best fitting model, according to AIC, has four ARCH lags.

Conduct ARCH Test

Represent the NASDAQ percent returns as residuals that fluctuate around a constant level by centering the returns. Store the returns in the timetable.

TT.Residuals_NASDAQ = TT.Returns_NASDAQ - mean(TT.Returns_NASDAQ);

Conduct Engle's ARCH test at a 1% significance level on the residual series Residuals_NASDAQ. Specify four lags for the test statistic.

StatsTbl = archtest(TT,DataVariable="Residuals_NASDAQ",Lags=lags,Alpha=0.01)StatsTbl=1×6 table

h pValue stat cValue Lags Alpha

_____ ______ ______ ______ ____ _____

Test 1 true 0 460.82 13.277 4 0.01

h = 1 and pValue = 0 rejects the null hypothesis and suggests that the evidence for ARCH(4) conditional heteroscedasticity in the NASDAQ percent returns residual series is strong.

Input Arguments

Name-Value Arguments

Output Arguments

More About

Tips

To draw valid inferences from the test, determine a suitable number of lags by following this procedure:

Fit a sequence of ARCH(L) models by using

arima,garch,egarch, orgjrmodels and its correspondingestimatefunction. Restrict each model by specifying progressively smaller ARCH lags (i.e., ARCH effects corresponding to increasingly smaller lag polynomial terms).Obtain loglikelihoods from the estimated models.

Evaluate the significance of each restriction by using

lratiotest. Alternatively, compute information criteria usingaicbicand combine them with measures of fit.

Residuals in an ARCH process are dependent, but not correlated. Therefore,

archtesttests for heteroscedasticity without autocorrelation. To test for residual autocorrelation, uselbqtest.GARCH(P,Q) processes are locally equivalent to ARCH(P + Q) processes. If

archtest(res,Lags=L)shows evidence of conditional heteroscedasticity in residuals from a mean model, consider using a GARCH(P,Q) model with P + Q =L.

References

[1] Box, George E. P., Gwilym M. Jenkins, and Gregory C. Reinsel. Time Series Analysis: Forecasting and Control. 3rd ed. Englewood Cliffs, NJ: Prentice Hall, 1994.

[2] Engle, Robert. F. “Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation.” Econometrica 50 (July 1982): 987–1007. https://doi.org/10.2307/1912773.

Version History

Introduced before R2006a