Main Content

3 results

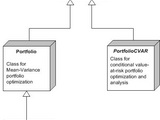

Object-oriented implementations of the Portfo and the Black-Litterman approach

BLScript.m

- The script BLScript.m is to support the Black-Litterman implementation

compareWeights( ExcessHistoricalReturns, ExcessImpliedReturns, sigma, mktCaps )

- compareWeights Helper function to compute and plot allocations

View(varargin)

- VIEW MATLAB code for View.fig

Code for the article in the September 2011 article http://www.wilmott.com/magazine.cfm

PriceArithmeticAsianOptionQuasi(S0,X,r,T,sigma,NSteps,NPaths,QuasiType)

- Function to compute Arithmetic Asian Option price ; Using Quasi Random

Readme.m

- The following files are MATLAB scripts that go with the article

PriceArithmeticAsianOptionFin(S0,X,r,T,sigma,NSteps,NPaths)

- Function to compute Arithmetic Asian Option price ; Using Financial

TimingScriptQuasi.m

- Timing script to test scripts using Quasi Random numbers

PriceArithmeticAsianOptionSDEZ(S0,X,r,T,sigma,NSteps,NPaths)

- Function to compute Arithmetic Asian Option price ; Using SDE and

PriceArithmeticAsianOptionV(S0,X,r,T,sigma,NSteps,NPaths)

- Function to compute Arithmetic Asian Option price ; Vectorized version

TimingScriptComparison.m

- Timing script comparing looped and Vectorized

PriceArithmeticAsianOption(S0,X,r,T,sigma,NSteps,NPaths)

- Function to compute Arithmetic Asian Option price ; Using Loops

PriceArithmeticAsianOptionSDEAntiThetic(S0,X,r,T,sigma,NSteps,NPaths)

- Function to compute Arithmetic Asian Option price ; Using SDE and

PriceArithmeticAsianOptionPCT(S0,X,r,T,sigma,NSteps,NPaths)

- Function to compute Arithmetic Asian Option price ; Using PCT

PriceArithmeticAsianOptionSDESolution(S0,X,r,T,sigma,NSteps,NPaths)

- Function to compute Arithmetic Asian Option price ; Using SDE and

TimingScriptSDE.m

- Timing script to test time taken for scripts using different SDE

PriceArithmeticAsianOptionSDE(S0,X,r,T,sigma,NSteps,NPaths)

- Function to compute Arithmetic Asian Option price ; Using SDE

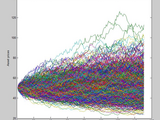

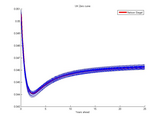

Developing Scenario Analysis Applications using Interest Rate Curve Objects in MATLAB

getRateScenariosN(NSModel,PlottingDates,n)

- getRateScenarios Helper function that returns n rate scenarios

IRFunctionCurve2

- LOCCONVERT Converts compounding and day count conventions

getNewNelsonsiegelParamsN(oldParams, t,n)

- getNewNelsonsiegelParams Helper function that returns new NelsonSeigel

getNewNelsonsiegelParams(oldParams, t)

- getNewNelsonsiegelParams Helper function that returns new NelsonSeigel

getRateScenarios(NSModel,PlottingDates,n)

- getRateScenarios Helper function that returns n rate scenarios

pctdemo_helper_getDefaults()

- PCTDEMO_HELPER_GETDEFAULTS Process the settings in PARALLELDEMOCONFIG.

scenarioanalysis.m

- Scenario Analysis demo to accompany the article "Navigating curves"

You can also select a web site from the following list

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom(English)

Asia Pacific

- Australia (English)

- India (English)

- New Zealand (English)

- 中国

- 日本Japanese (日本語)

- 한국Korean (한국어)